Quantum Advantage in Finance

- Quantum computing for finance is preparing to move from the research lab to commercial deployment, with major banks (HSBC, Vanguard, JPMorgan) already running quantum experiments on production data.

- The proprietary AQS Quantum Advantage Estimator tool, evaluating more than 20 quantum processors across multiple types of financial use cases, projects that IBM's Starling processor will achieve practical quantum advantage for some financial use cases, such as correlation modeling, by 2029. Competitors are seeking to meet or exceed IBM Starling performance levels in a similar timeframe.

- The AQS FabriQ platform delivers quantum-inspired risk analytics today, with a seamless upgrade path to true quantum hardware as it matures.

- The primary benefit of quantum computing for finance may be more accurate risk estimates, rather than calculation speedups. Better risk estimates may decrease capitalization requirements for banks.

1. Why Quantum Computing Matters for Finance Now

Three converging trends are making quantum computing commercially relevant:

- Hardware is crossing the utility threshold. Google's Willow quantum processor chip demonstrated below-threshold quantum error correction. IBM's Heron processors have started to approach production-level workloads. The question is no longer "will it work?" but "when will it work for my application?"

- Major banks are already investing. HSBC recently demonstrated quantum-enabled algorithmic trading, and Vanguard showed that quantum computing can help optimize bond portfolio construction. Over $40 billion has been invested globally in quantum computing; the amount continues to rise.

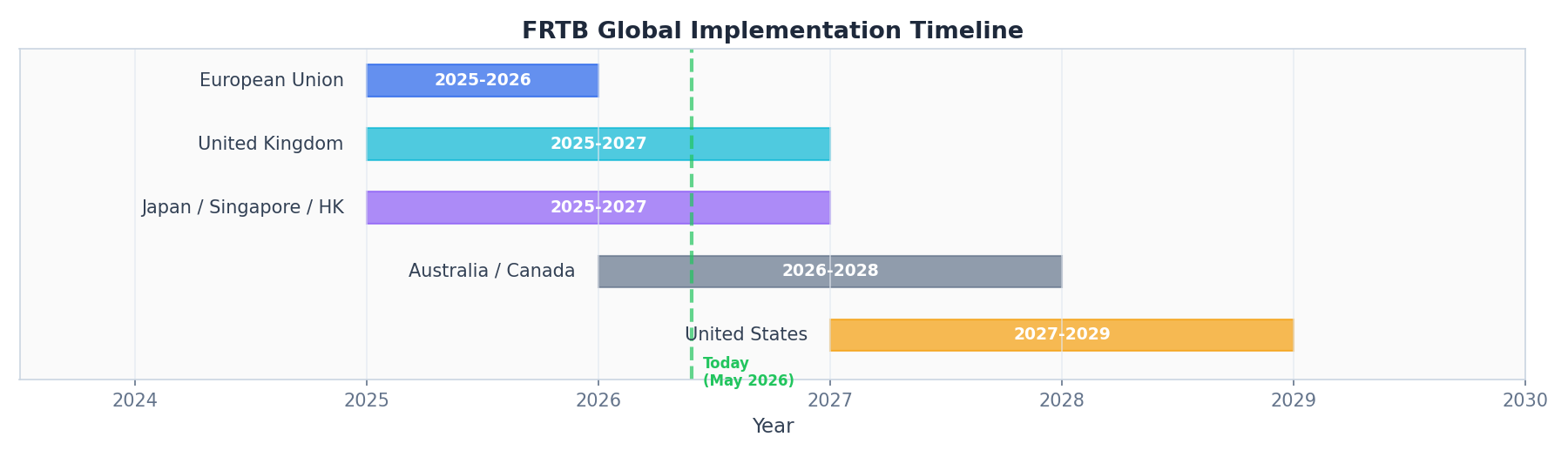

- Regulatory pressure is increasing. The Fundamental Review of the Trading Book (FRTB) mandates more sophisticated risk models globally, with EU compliance already live, and US implementation expected by 2027-2028.

FRTB regulatory implementation timeline by region.

McKinsey estimates quantum technology could create $2 trillion in value by 2035, with financial services among the primary beneficiaries. The problems finance faces, including risk analysis, portfolio optimization, and asset price modeling, are among the problem classes where quantum algorithms can provide proven mathematical speedups.

2. What AQS FabriQ Delivers Today

AQS FabriQ is a full-stack quantum finance platform, running on Google Cloud, that provides a Bloomberg terminal-style workspace for analysis and development teams in finance. Unlike research-oriented quantum computing platforms, FabriQ is designed for production deployment in regulated financial institutions.

The AQS FabriQ platform supports three computational approaches:

- Classical: Standard Monte Carlo simulation, historical simulation, analytical Value-at-Risk (VaR), etc. for benchmarking

- Quantum-inspired: Matrix Product State (MPS) tensor networks that capture fat tails in distributions, higher-order correlations, and regime-dependent behavior that classical models miss

- Native quantum: Quantum amplitude estimation, Grover search, and quantum generative models, able to execute on quantum simulators and quantum hardware now (e.g. with IBM Quantum Platform) for experimentation, and more reliably as processors mature

Quantum-Inspired: The Bridge Between Classical and Quantum Computation

Matrix product state (MPS) tensor networks, originally developed in quantum physics, are a technique for representing and deriving joint probability distributions, and can be used to model correlations of asset returns. Our backtesting with historical financial market data has demonstrated that MPS can effectively model higher-order correlations, which can produce more accurate risk predictions than either classical Gaussian Monte Carlo or historical simulation, with superior calibration of CVaR (conditional value-at-risk, also known as expected shortfall).

Critically, MPS is also a bridge to true quantum computing. Tensor network representations used for classical MPS training can be converted and loaded onto quantum devices for significantly faster processing. AQS customers who adopt this technology today will be able to seamlessly transition to quantum-native algorithms as hardware matures.

3. Why Not Build In-House?

A natural question for any technology leader is whether to build internally rather than adopt a vendor solution. In practice, three factors make this impractical for most financial institutions.

Specialized expertise that risk teams don't have

Implementing quantum techniques such as MPS correctly requires expertise in techniques from quantum physics, such as tensor contraction, bond dimension optimization, and alternating least squares training. Building an in-house MPS capability could require over 12 months of development and the hiring of staff with expertise in advanced physics or quantum information theory. Even then, the result would be a research prototype, not a production system.

A library of quantum algorithms is not a risk platform

A raw MPS implementation solves only one piece of the problem. A production-grade risk workflow requires market data ingestion, data preprocessing, model training pipelines, scenario generation, VaR/CVaR calculation, backtesting frameworks, visualization, and audit trails, all integrated into a workspace that analysts can use without a quantum computing background. AQS FabriQ delivers this complete stack, with a Bloomberg terminal-style interface designed for quantitative finance teams.

The window for early adopter advantage is now

The majority of investment funds, including large, sophisticated firms, still run Value-at-Risk calculations using classical Monte Carlo modeling or historical simulation. MPS-based risk analytics are not yet on most firms' radar. Organizations that adopt quantum-inspired methods today position themselves ahead of competitors and ahead of regulatory expectations, building institutional expertise before these techniques become mainstream.

4. When Will Quantum Advantage Arrive?

The AQS FabriQ Quantum Advantage Estimator is a proprietary analytical framework that evaluates more than 20 quantum processors from 17 vendors across 4 financial use case types. It helps answer a critical question: "When will quantum technology be useful for my specific application?"

Quantum hardware is advancing rapidly, with major milestones achieved in the last two years, such as Google's below-threshold error correction, Quantinuum Helios 99.9% gate fidelity, and IBM's Nighthawk architecture. The AQS Quantum Advantage Estimator tracks this progress and projects when each use case will cross the threshold for practical advantage.

| Milestone | Quantum Hardware | Expected Timeline | Theoretical Speedup for Relevant Use Cases |

|---|---|---|---|

| First practical quantum advantage | IBM Starling | 2028-2029 | 10x speedup for generative correlation modeling (small portfolios) |

| Broad advantage | Next-generation fault-tolerant hardware | 2033-2035 | 65-260x speedup for full-revaluation Value-at-Risk |

| Dominant quantum advantage | Future quantum processor | 2035+ | >100x speedup across various financial use cases |

5. Target Customer Base

AQS FabriQ is designed for quantitatively-driven financial institutions, where risk model accuracy directly impacts regulatory capital, portfolio performance, or both.

| Segment | Why Quantum-Inspired Risk Analytics Matter |

|---|---|

| Tier-1 Banks | FRTB compliance demands more sophisticated internal models. Better VaR calibration reduces capital add-ons under the Internal Models Approach (IMA). |

| Asset Managers | Multi-asset portfolios with complex correlation structures benefit most from higher-order dependency modeling. More accurate tail risk estimates improve drawdown management, client reporting, and client results. |

| Hedge Funds | Quantitative strategies require precise risk budgeting. MPS techniques (and eventually native-quantum algorithms) capture regime-dependent correlations that classical models miss, improving tail risk hedging and alpha preservation. |

| Trading Firms | Intraday risk recalculation speed is a competitive advantage. Quantum-enhanced VaR enables more frequent portfolio rebalancing and tighter risk limits. |

| Insurance | Asset-liability management and catastrophe modeling involve fat-tailed, highly correlated risks - the types of distributions for which MPS and quantum computing outperform Gaussian assumptions. Relevant to Solvency II compliance. |

Key decision-makers

Within these organizations, AQS FabriQ is typically evaluated by the Head of Quantitative Research (algorithm accuracy), adopted with approval from the Chief Risk Officer (regulatory capital impact), and integrated with sign-off from the Head of Technology (security, vendor governance). Innovation leads and quantum readiness teams are often the initial champions.

6. Why AQS

- Delivering value today: quantum-inspired risk analytics from AQS are running in production today with a regulated hedge fund

- Vendor-neutral: benchmarks algorithms across over 20 quantum hardware providers and platforms, with no lock-in

- Built-in data integration: algorithms run against financial market data from OneTick, KX, and other widely-used data platforms

- Seamless upgrade path: customers can adopt quantum-inspired solutions today and upgrade to native-quantum implementations when hardware matures; same platform, same user interface, same data

- Enterprise-grade: running on Google Cloud Platform with industry-standard security, auditability, and data governance

- Proprietary quantum algorithm IP: novel quantum training algorithms from AQS research & development

7. Next Steps

AQS FabriQ is available for evaluation. Every result presented in this document can be reproduced within the FabriQ platform, using production-level workflows with financial market data.

To learn more or schedule a demonstration:

© 2026 Applied Quantum Software (AQS) - San Mateo, California, USA

Quantum Computing for Enterprise Finance